Your trading platform communicates with your broker through encrypted connections. HTTPS—the same protocol protecting your banking sessions—encrypts your credentials and order data.

The question isn’t whether your connection is secure. The question is whether adding a VPN improves that security enough to justify the performance cost.

Understanding VPNs

A Virtual Private Network creates an encrypted tunnel between your system and a remote server. Your internet traffic routes through this server, masking your IP address and preventing local network observation.

How VPNs Work

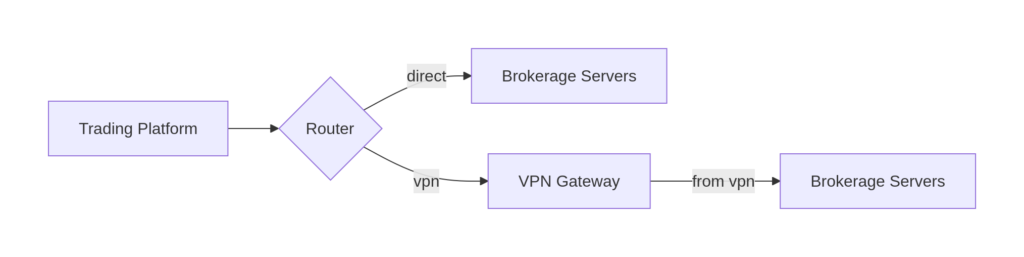

Your Computer → Encrypted Tunnel → VPN Server → Internet → Broker

vs. Direct Connection:

Your Computer → Internet → Broker (HTTPS encrypted)

The encryption difference: Both connections use encryption for data transmission. The VPN adds an additional encryption layer plus server intermediation.

What VPNs Provide

- IP address masking: Your broker sees the VPN server's IP, not yours

- ISP tracking prevention: Your ISP cannot observe your requested end route (browsing activity)

- Geolocation: VPN servers in differing regions enable regional network access

- Local Network Privacy: When set per client, others on your network cannot observe traffic

What VPNs Don't Provide

- Magic Security: If a site uses HTTPS (all good ones do), you're encrypted end-to-end already

- Complete Anonymity: Advertisers and data brokers use more tracing methods than simply IP

- Zero Latency: All VPN routes add proccessing time and server distance and hops

Security Foundation Already Present

Understanding HTTPS clarifies why VPNs provide marginal additional security for trading.

HTTP vs. HTTPS

|

Protocol |

Encryption |

Visibility |

|---|---|---|

|

HTTP |

None |

Entirely visible to intermediaries |

|

HTTPS |

TLS encryption |

Encrypted from your browser or software to the server |

|

VPN |

Various |

Encrypted from brower, system, or router to server |

HTTP transmits data in plaintext—anyone between you and the server can observe content. HTTPS encrypts data end-to-end. Your broker’s servers use HTTPS exclusively; your trading platform encrypts credentials and order data before transmission. VPNs wrap the existing package data with encryption for the VPN endpoint.

What This Means for Trading

Your trading platform already encrypts:

- Login Credentials

- Order Submissions

- Price Data Transmission

- Account Information

A VPN does not add functional encryption to this channel, merely it routes encrypted traffic through an additional networks and servers. Costing you time and caluclations.

Latency Cost

- Server Distance: Your traffic routes through the VPN server before even attempting to reach your broker

- Encryption Processing: VPN encryption/decryption adds processing overhead

- Server Congestion: VPN servers have bandwith and processing capacity limits that affect routing speed

|

VPN Configuration |

Typical Latency Addition |

|---|---|

|

Local VPN Server |

10-30ms |

|

Regional VPN Server |

30-70ms |

|

Distant VPN Server |

70-150ms+ |

For scalpers executing dozens of trades daily, even 20ms of additional latency compounds into substantial slippage costs.

Our Recommendation

For active trading: Do not use a VPN.

The security benefit is marginal. All trading platforms use HTTPS encryption. A VPN adds latency that directly impacts execution quality without providing meaningful additional protection.

Market vs. Limit Orders

The cost of VPN latency depends on your order type. Market orders and limit orders experience latency differently, and the cost calculation diverges substantially.

Market Orders: Execute at the prevailing ask or bid when the order reaches the exchange. Every millisecond of delay increases the probability that price moves against your order before execution. Latency manifests as direct slippage cost. The calculation is straightforward: delayed arrival means worse fill price.

Limit Orders: Specify a maximum (buy) or minimum (sell) price. The order does not execute if the market moves past your limit. Latency does not produce slippage on filled limit orders because price is specified. Instead, latency produces opportunity cost: the limit order arrives at the exchange after the price has already moved through your level, and the order goes unfilled or partially filled.

Market Order Math

Consider an active day trader executing 200 trades daily on ES futures contracts for demonstrative purposes:

|

Factor |

Without VPN |

With VPN(assume +30ms) |

|---|---|---|

|

Average slippage per trade |

~0.5 ticks ($6.25) |

~1 tick ($12.50) |

|

Daily slippage cost |

~100 ticks ($1,250) |

~200 ticks ($2,500) |

|

Annual slippage cost |

~25,000 ticks ($312,500) |

~50,000 ticks ($625,000) |

|

Additional annual cost |

-- |

~25,000 ticks ($312,500) |

Demonstrative example only. Assumes 200 trades per day, 250 trading days per year, ES futures ($12.50 per tick), and latency differential of 30ms. Does not account for broker commission structures, exchange fees, market maker rebates, spread variability across instruments, and volatility-dependent liquidity conditions. Actual slippage costs are determined by instrument, market conditions, order size, and broker execution quality.

This calculation illustrates why we recommend against VPN use during active trading. The privacy benefits do not justify the execution cost.

Limited Limit Order

Limit orders face a different cost function. Latency does not degrade the fill price, the limit protects that. But latency determines whether the order arrives at the exchange within the window when the price is available.

A limit order placed at $100.00 with 30ms of additional latency may arrive to find the market bid already at $100.05. The order does not execute at $100.00 because the opportunity window closed before the order reached the exchange. The trader experiences no direct dollar loss, they experience opportunity cost, a missed entry.

The cost of missed fills is measurable but probabilistic. On a volatile day, a trader using limit orders might lose 3–8% of intended fills due to latency-driven arrival delays. On a low-volatility day, near zero. Unlike market order slippage, which often compounds predictably per trade, limit order costs manifest as entries that may have triggered but did not.

The Combined Picture

|

Order Type |

Primary Cost |

Measurability |

Predictability |

|---|---|---|---|

|

Market Orders |

Slippage on Execution |

Direct Dollar Cost |

Linear with Trade Volume |

|

Limit Orders |

Missed or Partial Fills |

Probabilistic Entry |

Non-Linear, Volatility Dependent |

Regardless of which order type dominates your strategy, additional latency imposes a measurable cost. For market-order traders, that cost is direct and compounding. For limit-order traders, it is the cumulative loss of entries that should have captured but did not.

The privacy benefits of a VPN do not justify either cost function.

When VPNs Are Appropriate

International Traders

If your trading platform restricts access based on geographic location, a VPN enables connection through US-based servers. Traders traveling through South America, Europe, and Asia can use VPNs to access US-locked platforms.

This is an acceptable use case. Geolocation requirements are a legitimate business need; VPN latency is the cost of access.

Corporate Networks

Proprietary trading firms often require VPN connectivity for network security policies. If your firm’s infrastructure mandates VPN use, that requirement supersedes general recommendations.

Non-Trading Browsing

Using a VPN while browsing, checking email, or accessing non-trading applications provides legitimate privacy benefits without trading performance impact.

Broader Security Picture

VPNs address only one attack vector: local network observation and ISP tracking. Comprehensive trading security involves:

|

Threat |

Mitigation |

|---|---|

|

Broker account security |

Two-Factor authentication, unique passwords |

|

Phishing attacks |

Email verification, TLS/SSL certificates |

|

Malware |

Anti-Virus, System Security Updates, Backup Software |

|

Physical security |

Secure office/workspace, system lock policies |

|

Data loss |

System backups (whole partition/disk), offsite backup |

A VPN protects one vector. Comprehensive security requires attention to all vectors.

FAQ

Do I need a VPN for trading?

No. Trading platforms use HTTPS encryption—your credentials and orders are already secure. VPNs add latency (20-100ms+) that directly impacts execution quality. We recommend against VPN use during active trading.

What security does my trading platform already provide?

Trading platforms use HTTPS encryption, which secures your login credentials and order data during transmission. This is the same encryption level protecting banking and credit card transactions. Additional encryption through VPNs provides marginal security benefit.

What if my broker requires a VPN for their network?

Some institutional networks require VPN connectivity for security policies. If your trading environment mandates VPN use, that requirement is necessary for your specific infrastructure. Our general recommendation applies to traders with discretionary VPN choice.

Can I use a VPN for non-trading activities while trading?

Yes. VPN use for browsing, email, and non-trading applications provides privacy benefits without affecting trading performance. Run your trading platform on the direct connection while using VPN for other activities.

What security measures should I prioritize instead?

Focus on two-factor authentication on your broker account, regular backup verification (Paragon image backups), antivirus software, and secure physical workspace. These measures address more significant threat vectors than VPN use during trading.

Configure Your Trading Computer

Explore Falcon Preferred Professional Configurations

Learn About Our 5-Year Warranty

Or call our specialists: 1-800-557-7142 — U.S. Based Lifetime Support —